November 27, 2023

To write my recent Phenomenal World piece on the climate risk doom loop, I had to do a fair amount of background research into how others conceptualized the concept. I thought a lot about what I did and didn’t like about what I saw. And in studying the insurance industry and the damages of climate disasters to communities, I found lots of stories that captivated my attention. While I kept both of these caches of background knowledge out of my piece, I think they’re relevant enough to publish them as an appendix of sorts.

To get a sense of what I’m arguing about the climate risk doom loop and the insurance industry, read my piece first. This appendix only supplements that argument. Part 1 is about model design. Why did I design the schematics that I did? Part 2 is really just a laundry list of links that I did not use as evidence but found great quotes within. Hopefully both halves flesh out the rhetorical universe within which I’ve written my piece, and perhaps even give you new aspects of our climate crisis to investigate.

***

appendix part 1: model design

Not one of the following articles features a diagram of what a “climate doom loop” or, as I refer to it, a “climate risk doom loop” looks like:

The closest thing I have found to a resource that visualizes any version of the doom loop happens to be the World Bank, which, last year, published “Assessing Financial Risks from Physical Climate Shocks: A Framework for Scenario Generation.”

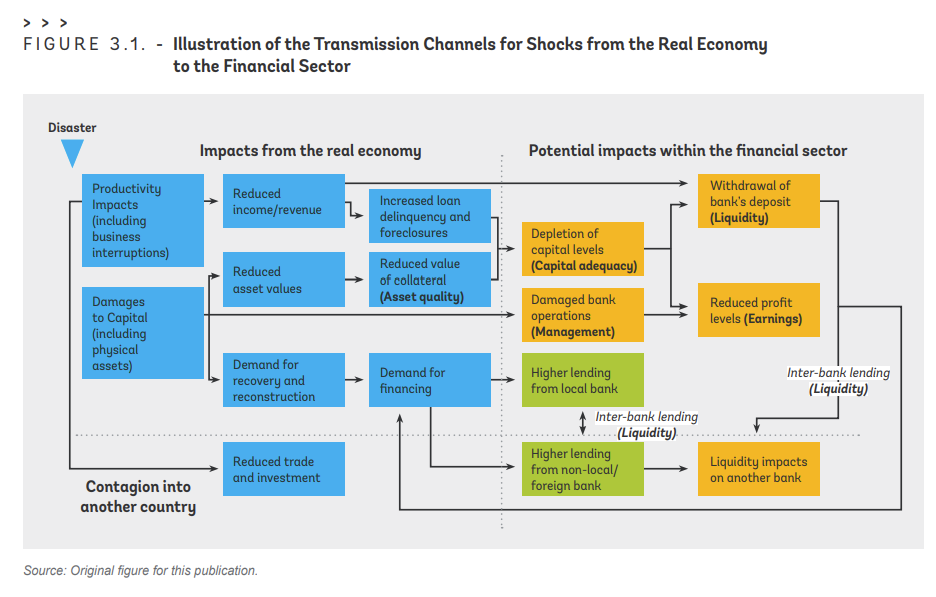

The report is a fairly dry piece of writing. But it does contain two diagrams that get really incredibly close to what I seek to explain. The first details how a shock propagates through the real sector and, subsequently, the financial sector:

For the most part, this diagram makes sense! I appreciate how granular it is. That’s not to say it gets everything right. I think it’s fair to argue that a disaster will impact the “real” and the “financial” sector at the same time, rather than one after the other, as this schematic implies. At risk of being uncharitable to its authors, it does not admit to the dual nature of capital investments as both fixed pieces of equipment with input costs and as financial assets with prospective yields. What this fact means, practically, is that it is very possible for a disaster in one country to reduce the expected yield or collateral value of most, if not all, capital investments in that country, even if none of that capital was damaged. While the first two columns of the schematic undoubtedly feed into the rest, a disaster can affect columns three through five even without input from the first two columns!

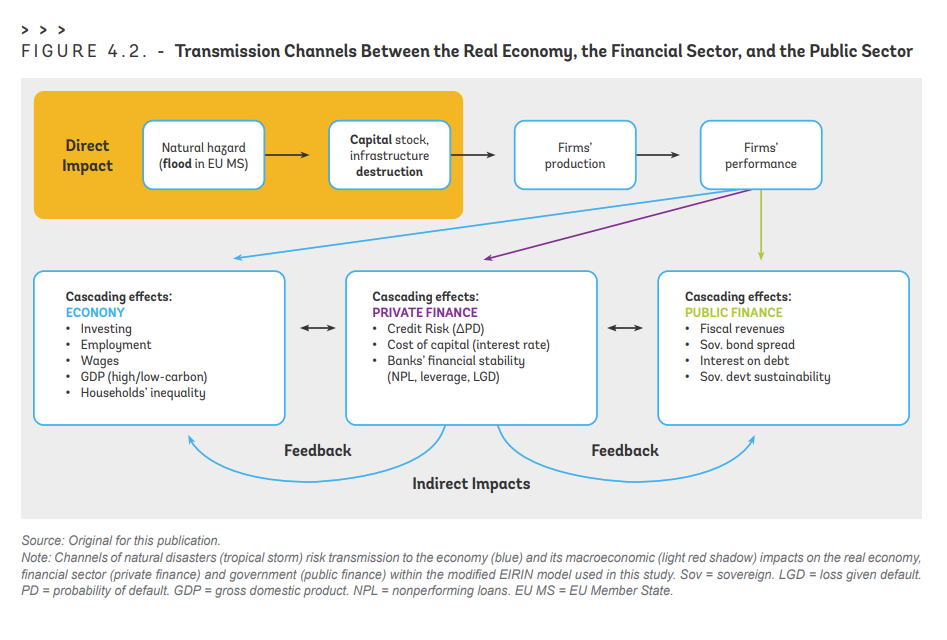

The other diagram that the report offers is more holistic, less granular:

This schematic is also sensible! But my previous argument still applies: even if a natural disaster did not destroy a country’s capital stock, it could still harm local credit and liquidity conditions.

Notwithstanding that critique, I find it interesting that the authors did not decide to draw their feedback loops back toward natural hazards and capital stock destruction. It seems as if they understand that a negative shock to firm performance will negatively impact public finances and the macroeconomic environment―but they do not take this insight a step further to admit that a worse macroeconomic environment makes it more likely for natural disasters and capital stock destruction to threaten firms.

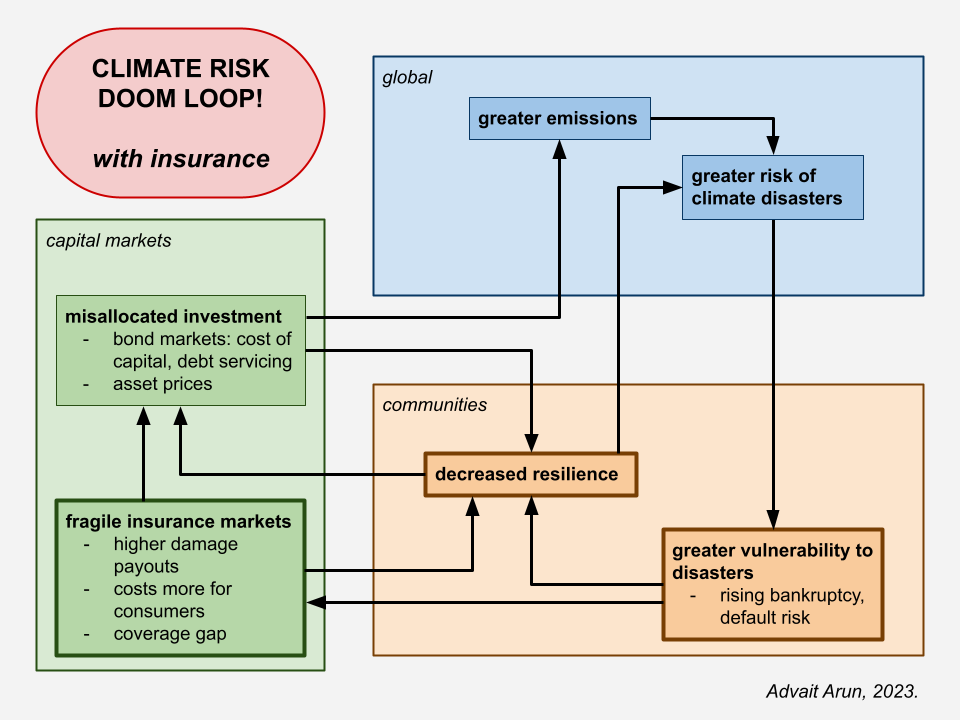

There’s precedent for treating natural disasters and catastrophes as exogenous acts of god. But the reality of climate change requires us to throw this assumption out the window. If the financial system produced yesterday’s capital stock, which produces today’s stock of emissions, which will produce tomorrow’s disasters, then there is no such thing as a climate disaster that is exogenous to the financial system.

The implications of treating climate change as endogenous to the workings of the financial system, then, not as a random external shock, are where my model begins:

This model includes insurance, of course, but its overall lack of granularity compared to the previous two schematics is intended to make it easier for a reader to understand the high-level interactions between capital markets, climate risks, and community resilience. I have designed it so that it does not contradict my argument here that disasters do not need to happen to a community for investment to flow away from it.

What does this detour into model construction mean for anyone working in “financial system decarbonization”? The answer, to me, is pretty simple: Decarbonization necessitates changing how the financial system allocates credit and liquidity to physical capital investments across the macroeconomy and to the emissions those investments generate. Perhaps the price signal can do that. Perhaps not. This is where the rubber hits the road.

***

appendix part 2: laundry list of links

(0) Our Insurance Dystopia | Boston Review

“As we think about how to imagine new insurance futures, we will have to reckon, in particular, with two broad features of insurance provision in the United States: the fraught relationship between the private insurance industry and the state, and the growing power of insurance companies in gathering and wielding data about individuals and groups. Each presents unique obstacles to the more utopian possibilities Royce envisioned.”

***

(1) Climate Destruction Fuels Growing Sector of the US Economy | Bloomberg

“Fallout from climate events tends to be highly inflationary at both the local and national levels, as goods and services are diverted to meet the immediate needs of affected areas, Stevenson says. The BI Repair Sector includes 37 companies that are focused on storage, rentals, waste removal, building products, materials and construction and heating, ventilation and air conditioning (HVAC) services.

The average stock in the group, which includes Home Depot and Waste Management Inc., outperformed an equal-weighted S&P 500 by 96% on “a total-return, beta-neutral basis” over the past 10 years, Stevenson says.

For example, shares of Advanced Drainage Systems Inc. almost quadrupled since the first half of 2020 at the same time the company’s revenue almost doubled, partly due to the rising amount of flooding near rivers and coastal cities. Advanced Drainage makes storm-water management and drainage systems.”

***

(2) One Bond Market Is Defying the Global Selloff With Record Returns | Bloomberg

“As bond markets everywhere get battered by a cocktail of higher interest rates, deficit angst and hawkish central bankers, one class of debt instrument is handing creditors double-digit returns: catastrophe bonds.

Investors in the $40 billion market for so-called cat bonds have literally been sitting out the storm to reap returns as high as 16% this year. Because of the way the bonds are structured, their coupons keep going up as Treasury yields rise, and investors get a sizable risk premium on their capital, as long as catastrophe doesn’t hit.

…

For now, many of the models underpinning the terms of catastrophe bonds focus on big hurricanes and earthquakes. But investors and issuers are going to need to figure out how to come up with equivalent models for wildfires and flash floods.

“There are concerns the modeling isn’t keeping up with those risks,” said Peter DiFiore, a managing director of Neuberger Berman, which oversees about $1.2 billion in cat bond investments on behalf of clients.”

***

(3) The Quest for the Low-Budget Park | Bloomberg

“The bargain-basement development of the Mission Boulevard park may serve as a useful model for park and recreation departments across the US that are facing elevated costs, just as a pandemic-era reappraisal of these public spaces has reaffirmed their importance and popularity. Steel, lumber, playground parts, asphalt, bathrooms and trees have all seen prices leap in line with general inflation and pandemic-era shortage and supply chain shocks, forcing officials to rethink and rebudget. Park and recreation facilities have wildly varying costs, depending on their locations and amenities. But every cost metric seems to be heading up.

…

Park equity gaps are especially pronounced in low-income urban as well as rural areas, with neighborhoods that are predominantly people of color and in low-income areas having roughly 40% less access to green space. While marquee projects in affluent areas might receive private funding, it’s harder to attract donor interest for more run-of-the-mill parks in poorer neighborhoods. But that’s where the need is most acute.”

***

““We are in a global race for capital,” said the chief executive of the Insurance Council of Australia, Andrew Hall, who accompanied Jones. Australia must “tell a better risk management story” by coordinating efforts at all levels of government to improve land-use planning and building codes, or insurance costs would rise further.

About a third of premium increases have come from a surge in reinsurance rates, which have risen by about a fifth in the past year to two-decade highs. Eastern Australia’s floods last year alone caused insured losses of $6.8bn, making it the county’s largest natural catastrophe claims event, SwissRe said.”

***

(5) US announces $3.5B for projects nationwide to strengthen electric grid, bolster resilience | AP

““As we sadly saw in California, aging electricity infrastructure can cause catastrophic loss of life, property, natural areas and forest fires,” said Jonathan Foley, executive director of Project Drawdown, a group that publicizes climate solutions.”

***

“In a climate shocked world, demand for such safe assets will only grow. And given the US’s rather ‘laissez faire’ attitude to public insurance and the inability of exporters to provide an alternative asset (they don’t import enough to become an alternative global currency) the US is the most likely place to be able, paradoxically, to afford exactly what the US does not want to fund – a welfare state. And even if they have to do that because of climate change, they will be able to, in part because everyone else will lend them the money.

…

If states generate debt to build assets that have a positive return (think quality public housing or renewable energy) then the net asset position of the state improves. Far from a fiscal crisis, the forthcoming catastrophe could be a fiscal boom where austerity is confined, finally, to the dustbin of bad ideas.

So I give two cheers to Hay’s catastrophism. The first for insisting that the future will not be like the past and that the tools of the past will not be fit for that future. The second for identifying the state as the ‘insurer of last resort’ and the problem of insuring the uninsurable as the hidden mission of the welfare state. But I diverge when it comes to thinking that the balance sheet logic of running a corner shop applies to states in moments of crisis, especially hegemonic states.

Hay argues that a generalized default is where we are headed. But I ask, who will ‘we’ default onto? Mainly ourselves, and we are all in this together. As the climate activists remind us, you can’t print another planet, but you can print money.”

***

“Geographers have interpreted the rise of weather insurance for small agricultural producers as emblematic of financialization’s inexorable march to capitalize the countryside. Yet this market has proved far less successful than advocates hoped or critics feared. Rather than a speculative tool for surplus extraction from smallholders or a mechanism for their financial subjectification, this article reinterprets weather insurance as an infrastructure of concessionary transfers from the development sector to make market-mediated mechanisms work. These transfers are emblematic of the new distributional terms struck between donors, states, and insurance capital as financial risk transfer is articulated with the extension of fragmentary safety nets. Economic field experiments with insurance have proliferated as venues in which the value of insurance is tested by both economists and experimenting subjects. Just as data from these trials have suggested some positive welfare impacts, they have also indicated target clients are unwilling or unable to pay full market price, thus performing a new justification for the perpetual presence of subsidies. Such transfers present opportunities for reinsurers to command rents through their control of large pools of capital and their interpretive authority over techniques for pricing risk under uncertainty. In a changing climate, reinsurers are poised to collect larger rents from donors’ and governments’ premium subsidies meant to decrease insurance costs for the vulnerable. These dynamics of rent cycling underscore the urgency of building more equitable, systematic risk-sharing infrastructures to replace the current fragmentary archipelagos of weather insurance.”

***

(8) Measuring the Climate Risk of Insurers | FRB of New York

“Insurance companies can be exposed to climate-related physical risk through their operations and to transition risk through their $12 trillion of financial asset holdings. We assess the climate risk exposure of property and casualty (P&C) and life insurance companies in the U.S. We construct a novel physical risk factor by forming a portfolio of P&C insurers’ stocks, with each insurer’s weight reflecting their operational exposure to states associated with high physical climate risk. We then estimate the dynamic physical climate beta, representing the stock return sensitivity of each insurer to the physical risk factor. In addition, using the climate beta estimates introduced by Jung et al. (2021), we calculate the expected capital shortfall of insurers under various climate stress scenarios. We validate our approach by utilizing granular data on insurers’ asset holdings and state-level operational exposure. Our findings indicate a positive association between larger exposures to risky states and higher holdings of brown assets with higher sensitivity to physical and transition risk, respectively.”

***

“Municipal bond markets begin pricing sea level rise (SLR) exposure risk in 2013, coinciding with upward revisions to worst-case SLR projections and accompanying uncertainty around these projections. The effect is larger for long-maturity bonds and is not solely driven by near-term flood risk. We use a structural model of credit risk to quantify the implied economic impact and distinguish the effects of underlying asset values and uncertainty. The SLR exposure premium exhibits a different trend from house prices and is unaffected by house price controls. Taken together, our results highlight the importance of climate uncertainty in driving municipal bond prices.”

***

“Counties more likely to be affected by climate change pay more in underwriting fees and initial yields to issue long-term municipal bonds compared to counties unlikely to be affected by climate change. This difference disappears when comparing short-term municipal bonds, implying the market prices climate change risks for long-term securities only. Higher issuance costs for climate risk counties are driven by bonds with lower credit ratings. Investor attention is a driving factor, as the difference in issuance costs on bonds issued by climate and nonclimate affected counties increases after the release of the 2006 Stern Review on climate change.”

***

(11) Fund Managers Are Updating Bond Models to Capture a New Risk | Bloomberg

“Barclays analyst Maggie O’Neal is among those to have spoken out about the potential for nature-related risks to trigger downgrades and dent portfolio values for bond investors who don’t react in time. And sovereign downgrades would in turn lead to higher borrowing costs, ultimately “compounding credit risk for bondholders,” she said in a September report.”

***

(12) ‘Catastrophe’ Bond Market Headed for Major Surge in Issuance | Bloomberg

“Even in some of the wealthiest corners of the world, there’s “not enough insurance coverage” to deal with the potential losses ahead, according to Petra Hielkema, chair of the European Insurance and Occupational Pensions Authority.

…

In general, however, Ineichen said there are some corners of the market that Schroders tries to be “strongly underweight,” such as flood and wildfire risk. “We do invest, but it’s marginal,” he said. “It brings a volatility that’s better suited to an insurance balance sheet, and we think the price is lagging in terms of the risk.”

If cat bond issuers want to entice investors to expose themselves to such risks, they’ll “have to increase their premiums,” Ineichen said.”

***

(13) Climate Change Will Test Tokyo’s World-Class Flood Defenses | Bloomberg

“Dramatic increases in the intensity and frequency of storms in recent years is testing the limits of the city’s existing system. Under the 2022 Tokyo Resilience Project, a 15-trillion-yen government plan to fortify the capital’s infrastructure against natural and man-made disasters, flooding was named one of the five most urgent threats alongside earthquakes, volcanic eruptions, power and communication failures and infectious diseases.”

***

(14) Nowhere Is Safe From Worsening Climate Change, New US Report Warns | Bloomberg

“The nation has already experienced a record-high 25 disasters this year that have generated at least $1 billion in damages each, from deadly wildfires in Maui to flooding in Vermont to Hurricane Idalia pummeling Florida. On average, according to the report, the US now experiences a billion-dollar disaster every three weeks, compared to once every four months (adjusting for inflation) in 1980, when the National Oceanic and Atmospheric Administration first started tallying records.”

***

(15) What Happens After the World Reaches Net-Zero Emissions? | Bloomberg

“The uncertainty is itself an argument for reducing emissions as quickly as possible. If any warming can be expected to follow the end of widespread emissions, countries will want to accelerate their plans and supercharge efforts to remove carbon dioxide from the atmosphere.

…

Emissions reductions are also likely to be gradual, and emissions impacts will last decades if not centuries. Regardless of temperature, many other aspects of Earth’s systems will continue to feel the effects of global warming long after achieving net zero. “Even in a world that stabilizes its global temperature, we would expect to see continued sea level rise, ecosystem changes, changes to ice sheet mapping, continued ocean warming and acidification of the ocean waters,” Palazzo Corner says.”